SP500 LDN TRADING UPDATE 14/11/25

SP500 LDN TRADING UPDATE 14/11/25

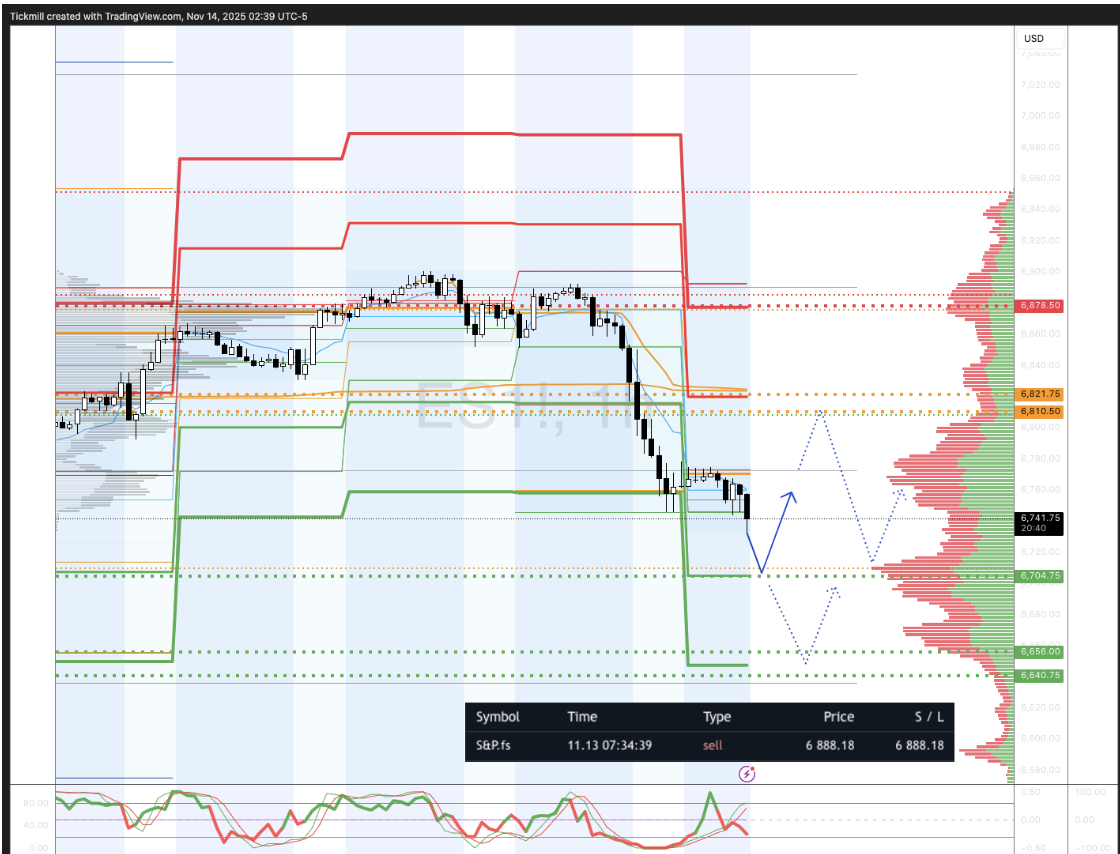

WEEKLY & DAILY LEVELS

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 6820/30

WEEKLY RANGE RES 6877/6629

NOV EOM STRADDLE 7054/6626

NOV MOPEX STRADDLE 6929/6399

DEC QOPEX STRADDLE 7054/6303

DAILY STRUCTURE – BALANCE - 6892/6746

DAILY BULL BEAR ZONE 6810/20

DAILY RANGE RES 6819 SUP 6705

2 SIGMA RES 68788 SUP 6648

DAILY VWAP BEARISH 6831

VIX BULL BEAR ZONE 18.5

TRADES & TARGETS

SHORT ON ON TEST/REJECT DAILY BULL BEAR ZONE TARGET DAILY RANGE SUP

LONG ON TEST/REJECT DAILY RANGE SUP TARGET DAILY BULL BEAR ZONE

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEWS

U.S. EQUITIES COLOR: UGLY

S&P closed down -166bps at 6,737 with a MOC of +$1.8b to Buy. NDX fell -205bps to 24,993, R2K dropped -285bps to 2,381, and the Dow declined -165bps to 47,457. Volume surged as 21b shares traded across all US equity exchanges, exceeding the YTD daily average of 17.3b shares. VIX rose +14% to 20.00, WTI Crude edged up +32bps to $58.68, US 10YR climbed +4bps to 4.11%, gold slipped -81bps to 4,179, DXY dipped -32bps to 99.18, and Bitcoin plunged -332bps to $98,514k.

Markets experienced sharp declines across the board, particularly impacting AI leaders and Momentum stocks under significant pressure. Weakness was attributed to a combination of factors: investors reducing exposure ahead of NVDA earnings next week, concerns raised by an FT article about a “phantom” data center issue inflating power generation demand, hawkish Fed commentary diminishing hopes for a December rate cut (Collins/Kashkari), additional corporate job cuts (e.g., Verizon today), and uncertainty surrounding upcoming macroeconomic data before the Fed meeting on 12/9.

The High Beta Momentum Pair (GSPRHIMO) dropped -6.4%, marking its second worst day of the year and its worst since DeepSeek (1/27). Notably, the last time Momentum declined ~7% in a single session, the VIX was at 45, compared to 20 today. Analysts highlighted that this momentum drawdown feels more severe due to its composition, as current momentum is more correlated with short interest, residual volatility, and beta, but less tied to quality compared to historical norms. AI and momentum stocks have traded closely together, with the pain concentrated on the long leg as buyers hesitate to engage in these themes. Non-thematic areas are attracting more activity instead.

Floor activity levels were moderate, rated a 5 on a 1-10 scale. The floor ended roughly flat compared to a 30-day average of -142bps. Despite the magnitude of market moves, single-stock activity remained orderly, showing no signs of panic. Long Only (LO) investors were net sellers at -$600m, driven by discretionary, tech, and macro products, while healthcare saw demand. Hedge Funds (HFs) were net sellers at -$1b, broadly across tech.

Bartlett noted increased LO activity in Semiconductors and AI, though the broader group remains rotational rather than seeing outright demand. The shift from September/October’s buyer-only flow to a more two-sided dynamic has contributed to choppier price action across AI, Tech, and Momentum over the past two weeks. Healthcare has emerged as a clear beneficiary of this rotation, with HFs using the sector as a correlation hedge against AI weakness. XLV rose for the ninth consecutive day, outperforming other sectors, excluding energy. HFs are actively buying healthcare, but longer-term investors have yet to step in.

Pharma strength continued, with GSHLCLCP up nearly +8% for the week. Key drivers include: (1) Pharma benefiting from negative correlations to AI winners at extreme levels, (2) LLY/NVO deals last week, (3) improved FDA clarity following the appointment of Pazdur to head CDER, (4) increasing generalist interest in the sector, and (5) institutional-led activity, with limited retail participation outside of LLY (TY Jon Chan).

Derivatives desks reported quiet flows despite the steep selloff and risk-off sentiment. Sellers of volatility were observed, with no significant demand for downside protection. The term structure continued to flatten, reflecting little fear further out on the volatility curve. Skew remained bid, while focus stayed on major rotations beneath the surface, highlighted by Momentum’s worst day of the year (-6.5%) since DeepSeek. Tomorrow’s straddle closed at ~0.87%.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!