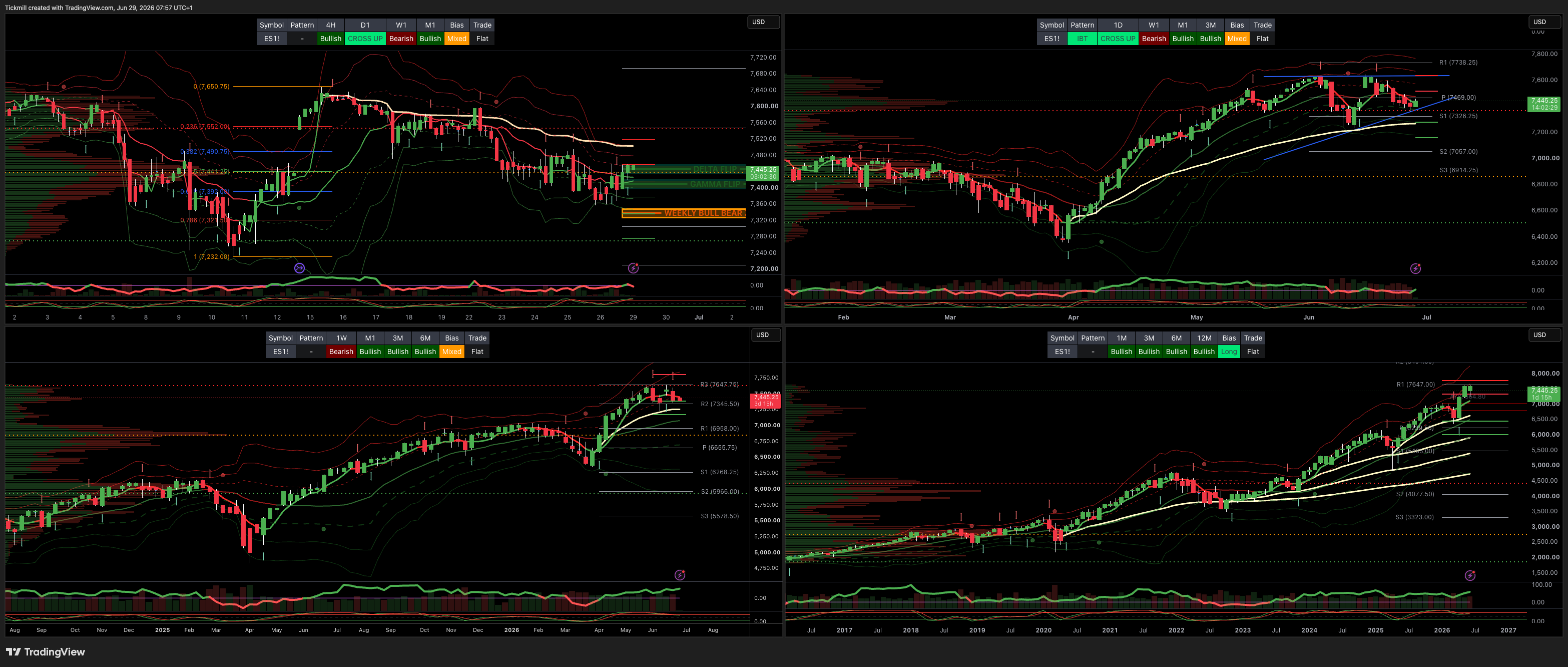

S&P500 Daily Action Areas & Price Targets 29/6/26

S&P500 Daily Action Areas & Price Targets 29/6/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7350/40

WEEKLY RANGE RES 7280 SUP 7520

MONTHLY RANGE RES 7932 SUP 7384

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.21 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 7417

WEEKLY VWAP BULLISH 7494

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - OTFL - 7459

WEEKLY STRUCTURE - BALANCE 7648/7247

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

GAMMA FLIP 7407

DELTA FLIP 7450

DAILY RANGE RES 7463 SUP 7330

2 SIGMA RES 7530 SUP 7264

VIX BULL BEAR ZONE 17.4

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY/MONTHLY BULL BEAR ZONE ***ACTIVE POSITION***

ACCEPTANCE ABOVE DAILY RANGE RES TARGET WEEKLY RANGE RES

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS FICC & EQUITIES TRADING DESK VIEWS

The key debate here is whether the latest cross-asset wobble is genuinely macro-led, or whether macro is being pulled around by equity-market internals. The instinctive answer would be to blame the shift on the end of the Iran conflict and the start of Warsh’s Fed tenure. Those are both meaningful macro junctures. Warsh’s first outing successfully established anti-inflation credibility, breakevens are falling, real rates are higher, the dollar has broken out, and equity volatility is rising again. That is exactly the sort of configuration that normally looks like a macro tightening impulse. But the better interpretation remains that this is still equities driving macro, not macro driving equities.

The most important evidence is that the stress is concentrated in the AI ecosystem rather than showing up as a broad macro liquidation. Korea is the cleanest example. The KOSPI traded limit down twice in the week, but that has to be contextualized against an index that had risen roughly 100% year-to-date before the halfway mark, has a 60% weighting to two stocks, and is heavily replicated by tens of billions of dollars in levered ETF products. In that kind of market structure, limit-down moves are not necessarily an exogenous macro event; they are an inherent feature of a market that has moved too far, too fast, with too much embedded leverage. The fact that half of Korea’s limit-down days this millennium have occurred in 2026, and 20% occurred in this week alone, says more about the extremity of the AI/memory positioning cycle than it does about a traditional macro shock.

The same conclusion holds in the US. The market is not rejecting AI as a theme; it is aggressively differentiating between the capex spenders and the capex recipients. Microsoft has made new 52-week lows and is now below its 2021 highs, while Amazon has broken below its 200-day moving average. Despite the broader enthusiasm around AI, the Mag7 are down more than 5% year-to-date as the market increasingly questions the ROI, margin implications, and duration of hyperscaler capex. The underperformance is even more pronounced across Asia, where China capex spenders such as Tencent, Alibaba, and Xiaomi are down sharply year-to-date. This is not a simple anti-growth or anti-tech move; it is a repricing of who pays for AI versus who gets paid by AI.

That value-transfer theme became even clearer as the market started to punish companies facing margin pressure from the memory squeeze. Apple and Dell both fell more than 5% as Apple, PlayStation, and others announced price hikes to offset higher memory costs. The implication is straightforward: Micron’s record gross margin is someone else’s cost inflation. Customers across the technology supply chain are paying up for scarce memory, and the equity market is now explicitly pricing the winners and losers from that bottleneck. This is why memory, storage, equipment, and upstream AI infrastructure have worked while hyperscalers, hardware assemblers, and platform companies with capex or input-cost pressure have lagged.

The irony is that there is still very little evidence of a meaningful slowdown in AI investment intent. The investment boom is not ending. If anything, capex plans remain large, demand visibility remains strong, and the AI infrastructure buildout still looks historic. But equity markets are now shifting from a simple “AI is good for everyone” framework to a more discriminating view of the profit pool. Investors are rewarding companies that receive the spend or benefit from scarcity pricing, while punishing companies that fund the spend or absorb the margin pressure. The volatility is therefore less about the end of the AI cycle and more about a possible shift in perception around the net winners and losers.

Micron sits at the center of that debate. Its margin evolution will likely become a business school case study because the memory industry’s post-GFC consolidation materially changed the trough-margin structure of the business. The market has rightly rewarded evidence that the industry has become more disciplined, more consolidated, and structurally more profitable through cycles. But the industry is still cyclical. Record gross margins and SK Hynix’s capex plans are both bullish and bearish depending on the time horizon. They validate the current shortage and pricing power, but they also signal the supply response that eventually eases bottlenecks. In aggregate, more supply is positive for the AI ecosystem because it removes a constraint. But it is negative for the most crowded beneficiaries of the bottleneck if investors begin to discount peak margins.

That is the key tension in memory. The market wants to capitalize the current shortage, but the very profitability of the shortage incentivizes the capacity that ultimately undermines it. Samsung and SK Hynix investment plans should eventually improve supply and reduce the pressure on downstream customers, which is beneficial for hyperscalers, device makers, and AI adoption more broadly. But for the stocks that have been bid aggressively on the scarcity narrative, this creates a classic cyclical risk: the best fundamentals may coincide with the market beginning to debate the peak.

The second related issue is the politics of AI. As the US moves toward midterms, the industry’s inability to articulate a compelling positive-impact narrative is likely to matter more. The data on employment is mixed. Tech’s share of total employment has been trending lower for more than five years, and the absolute job losses attributed to the sector are still small in the US data, around 11k per month. But job losses explicitly attributed to AI appear to be accelerating, and the industry has not yet offered a persuasive counter-narrative supported by data. If the political conversation shifts from productivity and innovation to job displacement and margin capture, that could add a new source of headline risk for AI leaders.

This matters because the equity market’s tolerance for AI capex and AI margins depends partly on the broader social and political narrative. When AI is framed as a productivity boom, high capex and high supplier margins are easier to justify. When AI is framed as job displacement, pricing power, and margin pressure for consumers and businesses, the narrative becomes more fragile. The market may not care immediately, but the summer and midterm calendar create more opportunity for that debate to enter the investment conversation.

The positioning work is the third and most immediate risk. Crowdedness is not, by itself, a reason to be bearish. Crowded trades can keep working if fundamentals keep improving. But crowdedness raises the penalty for any change in the fundamental narrative, and AI is now extremely crowded across multiple expressions. Hedge fund gross leverage is at new highs. Hedge funds have been aggressively net selling the US year-to-date to buy Asia, particularly Japan, Taiwan, and Korea, not China. Since ChatGPT, hedge fund net length first built in semis, then power and data centers were added in even larger size, and from the second half of last year memory net length has been added at roughly twice the size of semis or power plays.

Performance adds another layer of fragility. Hedge fund returns across fundamental, systematic, and multi-manager platforms have been excellent, with YTD gains in the 14–18% range. That creates less desperation, but also more incentive to protect gains into summer. Systematic and multi-strat funds are reportedly making more alpha in non-AI names than AI names, which suggests their return streams are somewhat diversified. Fundamental hedge fund performance, however, is almost entirely AI-driven, with non-AI adding no alpha. That is the more vulnerable cohort because if the AI profit-pool narrative shifts, the alpha engine becomes exposed.

The geographic correlation is also important. US and Asia AI exposure is driving returns, while Europe has not performed in the same way. US and Asia performance drivers have rarely been this correlated, reportedly in the 99th percentile. That means what looks like geographic diversification may actually be one common AI factor expressed through different markets. Korea, Taiwan, US semis, memory, power, data centers, and hyperscaler suppliers may all appear different in index terms, but they are increasingly the same trade from a portfolio-risk perspective. That is why Korea’s volatility matters so much for US investors: it is not a local event if the same AI factor is embedded across books globally.

This also explains why Europe and the UK may eventually regain diversification value. If the dominant risk in global equity portfolios is crowded AI exposure across the US and Asia, then markets with less direct AI factor exposure can become useful again. It is easy to forget that the UK significantly outperformed during the 2022 bear market, precisely because it had different sector composition, cheaper valuations, and less exposure to long-duration growth. The fact that Stoxx 600 has already outperformed the S&P halfway through the year is a reminder that non-US diversification can matter again when the US leadership complex becomes crowded.

The UK is not ready for a clean bullish call yet, but it is worth watching through the summer. The political situation is unsettled after the loss of another Prime Minister and the ten-year anniversary of Brexit. There is a real risk of a leftward lurch within Labour’s large governing majority, but there are also credible economic advisers around Andy Burnham, and the fiscal constraint should once again focus attention on growth as the only viable solution to limited spending capacity. The UK is deeply out of consensus, which is precisely why it could become interesting if the political path stabilizes.

The market response in the UK has been notable in its calm. Gilt yields are lower on the week, sterling is flat, and there is very little investor discussion of the upside possibility in the domestic economy. That asymmetry matters. It is too early to make the bet aggressively, particularly without a settled Prime Minister, but the ingredients for a contrarian opportunity are forming: extreme pessimism, fiscal constraints forcing a growth agenda, valuation support, and diversification value versus crowded US/Asia AI exposure.

Bringing this back to the original question, the Warsh wobble is real in the sense that the macro backdrop has changed. A newly credentialed hawkish Fed Chair, falling breakevens, higher real rates, a stronger dollar, and rising equity vol are not irrelevant. They tighten financial conditions at the margin and reduce the tolerance for speculative excess. But they are not the primary driver of the current market dispersion. The epicenter is equity-market structure: AI crowding, memory bottlenecks, hyperscaler capex concerns, margin pressure, Korea leverage, and the reallocation from spenders to recipients.

That distinction matters for portfolio construction. If this were a pure macro shock, the correct response would be to reduce beta broadly, buy duration defensives, and treat the move as a Fed-driven tightening. But if equities are driving macro, the better response is to re-underwrite the AI profit pool and reduce exposure to the most crowded and vulnerable parts of the theme, while maintaining exposure to secular investment beneficiaries and adding diversification where the AI factor is less dominant. The issue is not whether AI capex is ending; it is whether the market has misallocated too much capital to the wrong parts of the AI chain.

The tactical conclusion is that AI remains a historic investment boom, but the equity market is becoming more discerning and more volatile around it. The winners are those receiving capex, benefiting from scarcity, or enabling the buildout through memory, equipment, power, networking, custom silicon, and infrastructure. The losers are those funding capex with uncertain ROI, absorbing higher input costs, or facing margin compression. But even among the current winners, especially memory, the market must now contend with cyclical peak-margin risk and extremely crowded positioning.

So the answer is no, this does not look primarily like a Warsh wobble. Warsh and the end of Iran are the macro backdrop, but the dominant market impulse remains equity-led. The macro variables are responding to a change in leadership, crowding, and profit-pool perception within AI. The next phase is likely to be less about whether to own AI and more about which side of the AI ledger to own: the spenders, the recipients, the bottleneck beneficiaries, or the eventual beneficiaries of easing bottlenecks. That is a more complex market, but not necessarily a bearish one.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!